Building resilience through diversification

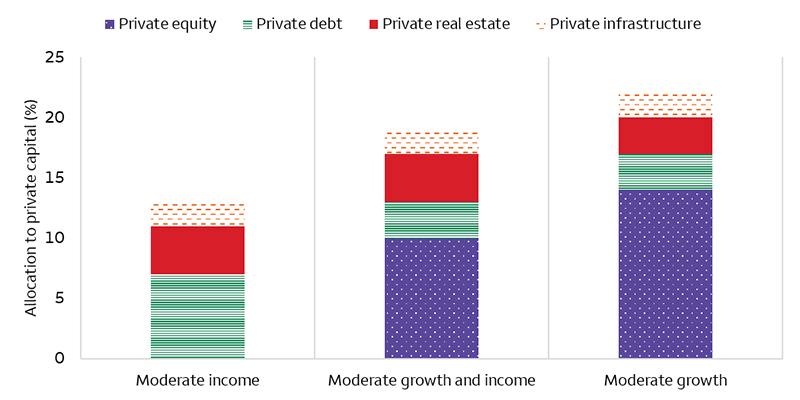

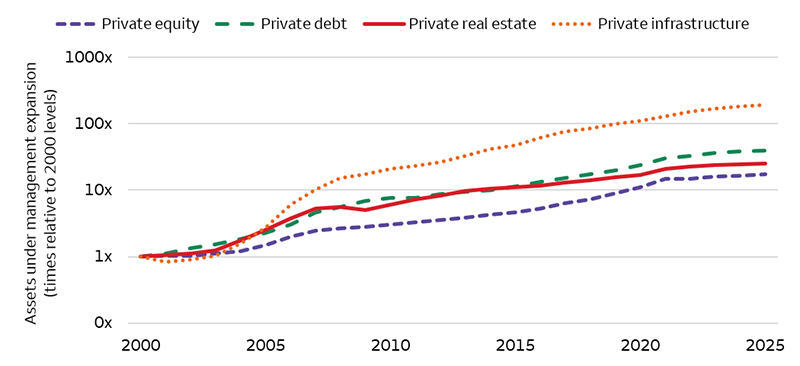

Our strategic allocations designed for qualified investors continue to allocate between 10% and 25% to private capital, highlighting the importance of alternative investments in diversified portfolios (see chart 1). This year, in addition to allocations across private equity, private debt, and private real estate, the illiquid strategic allocations also introduced private infrastructure as a new asset class. This addition reflects the continued growth of the private infrastructure market, both in assets under management and the range of strategies available (see chart 2).

Chart 1. WFII’s illiquid strategic asset allocations allocate between 10% and 25% to private capital

Sources: Wells Fargo Investment Institute (WFII). Data as of July 16, 2026. Based on WFII’s 2026 Illiquid Strategic Asset Allocation. Moderate investment objectives are used in the chart.

More broadly, we believe diversification should include differentiated investment strategies. A diversified private market portfolio may help improve resilience, manage risks, and support long-term return potential across a variety of market and economic environments.

Within private equity, we believe qualified investors can benefit from diversifying across company life stages. Buyout strategies, which typically invest in established companies, may serve as a core component of a private equity allocation. Growth equity and venture capital strategies, which focus on early-stage companies with significant expansion potential, may be used as additional positions for qualified investors who seek additional long-term return potential and can tolerate a higher level of risk.

Chart 2. Private infrastructure has grown significantly in assets since 2000

Sources: Wells Fargo Investment Institute and Preqin. Data as of December 31, 2025. Assets under management expansion is shown as a ratio relative to the level in 2000 for each asset class.

Qualified investors may also consider diversifying across investment types. Primary private equity exposure is often obtained through professionally managed funds that invest directly in a group of private companies, which may provide targeted industry and thematic exposure. In addition, secondaries and co-investments have become more widely available through the perpetual fund structures. Secondaries involve purchasing existing interests in private equity funds and may provide diversification across managers, industries, and investment vintages. Co-investments allow qualified investors to invest alongside fund managers and may offer lower fee structures than other private equity investments. Combining different investment types may help create a private equity portfolio with a balanced return, risk, and fee profile.

We believe corporate direct lending strategies may continue to serve as a core private debt holding given its historically resilient performance and limited defaults. However, as credit conditions evolve and private debt markets continue to expand, qualified investors may benefit from diversifying beyond direct lending into other segments of the market, such as private credit secondaries and asset-based lending. Private credit secondaries can offer exposure across a broad range of lenders, industries, and loan maturities, while potentially benefiting from ongoing elevated redemptions and portfolio rebalancing in the direct lending market. Asset-based lending focuses on loans secured by physical or financial assets and may provide differentiated income streams and additional downside protection through collateral.

Within private real assets, we continue to hold a constructive view on private infrastructure. We believe the asset class may benefit from several long-term trends such as digitalization and energy transition, as well as the demand for inflation-hedged income-producing assets.

Within private real estate, qualified investors may also consider diversifying beyond core real estate equity strategies. Real estate debt strategies, for example, may provide attractive income potential and portfolio diversification. We believe this may be particularly relevant as real estate markets continue to adjust to elevated interest rates, uneven economic growth, and differing supply-and-demand conditions across property sectors.

Overall, we believe qualified investors may benefit from taking a diversified approach across private market asset classes, strategies, and investment types to help build portfolios that can adapt to changing market conditions over time.

Alternative investments, such as hedge funds, private equity, private debt and private real estate funds are not appropriate for all investors and are only open to “accredited” or “qualified” investors within the meaning of U.S. securities laws.

Trading surge boosts banks despite margin risks

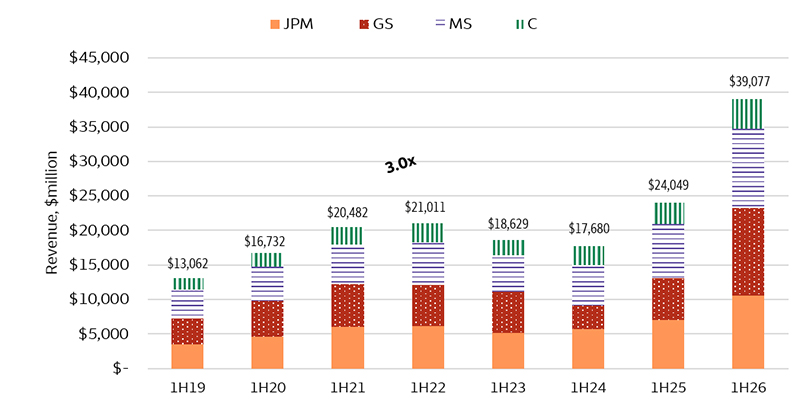

Trading and capital markets results at our recommended banks came in well ahead of expectations this quarter, pushing aggregate first-half equities trading revenue to a record $39 billion. While revenue has not increased every year, the nearly threefold increase from 2019 suggests the industry’s capital markets businesses have become more important earnings contributors, in our view. Although strong trading results have historically been associated with periods of heightened volatility, including the Iran-war-related volatility through the first half of this year, the persistence of the current cycle suggests something more structural may be occurring.

Equities trading revenue exceeded expectations across major banks this quarter, benefiting from elevated client activity, stronger derivatives and financing demand, and continued growth in institutional market participation. For equity investors, the trend suggests diversified banks may be less dependent on net interest income than they were prior to the pandemic.

The principal offset remains the macroeconomic backdrop. Higher oil prices, elevated long-term rates, and uncertainty around Fed policy could pressure net interest margins or eventually weigh on credit quality. However, those risks remain manageable today and have not meaningfully disrupted client activity.

Overall, trading strength has been the defining Financials sector earnings theme this quarter and, in our view, may help support earnings when traditional banking revenue growth slows.

Chart 3. First half equities trading revenue

Sources: Company earnings supplements and quarterly earnings releases for JPMorgan Chase, Goldman Sacs, Morgan Stanley, and Citigroup, 1H19–1H26. 1H = first half. JPM = JPMorgan Chase. GS = Goldman Sacs. MS = Morgan Stanley. C = Citigroup. These companies in the Financials sector represent all the companies on WFII’s Recommended lists that have equities trading revenues.

How states strengthen school bond credit

State school bond enhancement programs can improve the investment profile of school district bonds by providing an additional layer of credit support beyond a district's standalone credit quality. These programs often result in higher credit ratings, stronger market access, and improved secondary market performance, making enhanced bonds more attractive to a broader range of municipal investors.

For investors, the benefits extend beyond credit quality. Higher-rated bonds generally offer greater protection against adverse credit events and may benefit from improved liquidity. Enhanced school bonds frequently trade at lower yields and higher valuations than comparable unenhanced issues, particularly among smaller districts that may have limited market visibility. Common enhancement structures include state aid intercept, guaranty, appropriation, and permanent fund programs, though the level of support varies by structure. State aid intercept programs allow the state to redirect school funding dollars to bondholders if a district misses a payment, while guaranty programs generally represent a more direct state commitment to ensure timely debt service. Appropriation-backed programs rely on continued legislative approval of funds, while permanent fund programs pledge dedicated state trust or reserve assets as an added source of repayment support. Intercept programs are the most widely used, while guaranty and permanent fund structures typically provide the strongest support. Examples of enhancement structures include guaranty programs in Michigan and Utah, appropriation-backed programs in Minnesota and South Carolina, permanent fund programs in Texas and Nevada, and state aid intercept programs in Ohio, Missouri, Colorado, and Georgia. Each of these provides varying levels of credit support designed to strengthen bondholder security.

The expansion of state enhancement programs in the charter school sector may create additional investment opportunities for municipal investors. Charter schools often face greater operating and revenue risks than traditional school districts. State-backed enhancement programs can help mitigate some of these concerns by providing additional credit support and potentially supporting stronger credit ratings.

Although enhancement programs have rarely been called upon to make debt service payments, investors should continue to evaluate both the underlying issuer and the specific enhancement framework when assessing credit risk and relative value.

Oil’s round trip and back

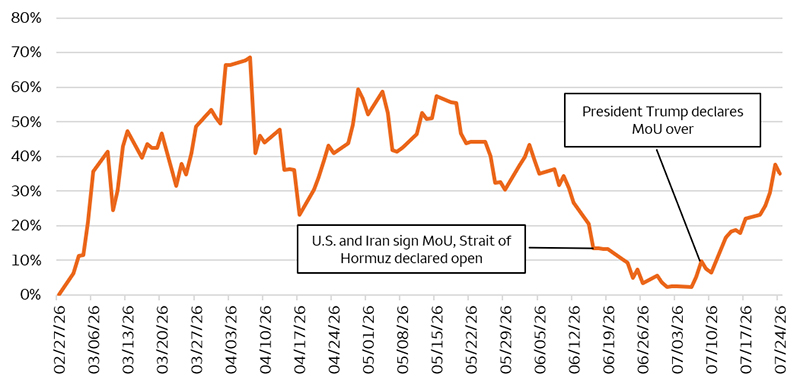

Geopolitics have dominated energy commodity prices this year. The Strait of Hormuz is a critical chokepoint for global energy supply, and the ongoing conflict between the U.S. and Iran has created a historically unprecedented level of supply disruption. Several buffers have helped partially mitigate disruptions to oil supply, though some may not be sustainable. The longer that the conflict continues, tail risks become more prevalent.

We expect the Strait to reopen, at least partially, before year-end, as escalating military pressure has failed to achieve its objectives while increasing economic strain on both sides. Prior periods of de-escalation during the conflict suggest both sides may be approaching their tolerance for economic stress. However, the details of any agreement will be critical to the oil price outlook, particularly with respect to the control structure of the Strait. In any de-escalatory outcome, it will take time for flows and activity to normalize relative to the pre-war environment. For this reason, we were surprised to see oil prices briefly return to pre-war levels in early July.

Whenever the conflict winds down, we expect a period of continued friction before the supply environment normalizes. Our year-end West Texas Intermediate (WTI) oil price forecast of $80 – $90 per barrel includes a geopolitical risk premium to account for factors such as higher shipping and insurance costs for oil tankers, the potential for periodic logistical disruptions, and a possible period of elevated demand as some countries step up purchases to refill depleted inventories. Until another peace agreement is reached, we acknowledge the potential for oil prices to trade above our year-end range, as supply buffers remain tenuous and disruptions have broadened to include alternative shipping lanes through the Red Sea.

Chart 4. Percent change in oil prices since start of Iran war

Sources: FactSet and Wells Fargo Investment Institute. Chart represents the percentage change in WTI oil price, indexed to 0 on February 27, 2026. WTI oil price at February 27, 2026, was $67.02 per barrel. WTI = West Texas Intermediate. MoU = Memorandum of Understanding.

Cash Alternatives and Fixed Income

intentionally blank

intentionally blank

intentionally blank

| Most Unfavorable |

Unfavorable |

Neutral |

Favorable |

Most Favorable |

|

intentionally blank

|

- Developed Market Ex-U.S. Fixed Income

- U.S. Long Term Taxable Fixed Income

|

- Cash Alternatives

- Emerging Market Fixed Income

- High Yield Taxable Fixed Income

- U.S. Intermediate Term Taxable Fixed Income

|

- U.S. Short Term Taxable Fixed Income

|

intentionally blank

|

Equities

| Most Unfavorable |

Unfavorable |

Neutral |

Favorable |

Most Favorable |

|

intentionally blank

|

|

- Developed Market Ex-U.S. Equities

- Emerging Market Equities

- U.S. Mid Cap Equities

|

|

intentionally blank

|

Real Assets

| Most Unfavorable |

Unfavorable |

Neutral |

Favorable |

Most Favorable |

|

intentionally blank

|

intentionally blank

|

- Digital Assets

- Private Real Estate

|

- Commodities

- Private Infrastructure

|

intentionally blank

|

Alternative Investments**

| Most Unfavorable |

Unfavorable |

Neutral |

Favorable |

Most Favorable |

|

intentionally blank

|

intentionally blank

|

- Hedge Funds—Equity Hedge

- Hedge Funds—Macro

- Hedge Funds—Relative Value

- Private Equity

- Private Debt

|

|

intentionally blank

|

Source: Wells Fargo Investment Institute, August 3, 2026. Please see Wells Fargo Investment Institute's Asset Allocation Strategy Report for more detailed, investable ideas in each asset group.

*Tactical horizon is 6-18 months

**Alternative investments are not appropriate for all investors. They are speculative and involve a high degree of risk that is appropriate only for those investors who have the financial sophistication and expertise to evaluate the merits and risks of an investment in a fund and for which the fund does not represent a complete investment program. Please see end of report for important definitions and disclosures.