May 6, 2026

Brian Rehling, CFA

Co-Head of Global Fixed Income Strategy

Mason Mendez

Investment Strategy Analyst

Harsh Agarwal

Investment Strategy Analyst

Central Bank Digital Currencies – What investors should know

Key takeaways

- Central bank digital currencies (CBDCs) are digital forms of a country’s official fiat currency (physical cash) issued directly by a central bank.

- Governments worldwide are actively exploring CBDCs, with much of the progress occurring outside the United States — most notably in China and several emerging markets.

- CBDCs have the potential to improve payment efficiency (which we think of as faster processing, smoother settlement and reduced operational frictions if adopted) — particularly in cross-border settlements through modernizing financial infrastructure and expanding financial inclusion to unbanked populations globally.

- At the same time, their development raises important questions related to privacy, financial stability, and governance, making the topic a central focus for policymakers and market participants alike.

Introduction

The exchange of value has evolved over centuries — from barter and commodity money to coins, paper currency, and electronically mediated payments. Each transformation has aimed to improve efficiency, security, and trust while supporting economic growth. Although modern payment systems are increasingly digital, they remain built on frameworks originally designed for physical cash and to occur between banks.

CBDCs represent a potential next step in this evolution. By offering a digital form of sovereign money issued and backed by the central bank, CBDCs seek to modernize payment infrastructure, improve cross border settlement, expand financial inclusion, and enhance the transmission of monetary and fiscal policy under certain design frameworks. While many countries have accelerated CBDC research and pilot programs, approaches vary significantly. The United States, in particular, has moved more cautiously due to privacy, governance, and financial stability concerns. Understanding the design, benefits, and risks of CBDCs is therefore essential to assessing their long-term implications for the financial system.

What Are CBDCs?

A CBDC is a digital form of a country’s official fiat currency. Although the legal structures and technological implementations vary across jurisdictions, most retail-oriented CBDCs are issued and are exchangeable for a country’s official fiat currency. As a result, they are designed to function as a digital equivalent of physical cash. Generally, holding a CBDC represents a direct claim on the central bank, just as holding physical paper currencies does today.

CBDCs differ fundamentally from cryptocurrencies, such as Bitcoin or Ethereum.1 Most cryptocurrencies are decentralized and privately issued (not issued by a government or central bank). In contrast, CBDCs are centralized and operate within a country’s regulated monetary system. They are issued by the central bank, governed by public institutions, and integrated into existing financial frameworks.

In addition to being digital representations of sovereign money, CBDCs can incorporate programmable features, allowing conditions such as expiration dates or spending restrictions to be embedded directly into the currency. These features would generally be designed to support policy objectives such as ensuring that public assistance funds are only spent on approved items like food and rent. They are also traceable, as transactions can be recorded using distributed ledger or similar technologies.2 In summary, CBDCs are designed to integrate directly with the state’s financial system, reflecting their role as a core component of modern monetary infrastructure rather than an alternative system operating alongside it.

CBDCs compared with existing digital money

While CBDCs are digital, they are distinct from the digital money already widely used today, such as bank account balances and electronic payments. For example, when individuals hold funds in a bank account, they are effectively holding a claim on that bank rather than on the state. And if an individual transfers money to someone else, while the electronic transfer is in process it is a liability of one (the paying) bank and an asset of the other (receiving) bank.

CBDCs differ in that the central bank creates digital equivalents of the national currency which are then distributed utilizing one of the different models shown in Table 2. In this sense, CBDCs are a digital version of physical cash rather than an evolution of private bank money, which has historically been the basis of electronic payments . Using the same example of holding funds in a bank account above, under a direct CBDC model (see Table 2), individuals are effectively holding a claim on the state rather than the bank. Although both systems facilitate electronic transactions, this distinction has meaningful implications for financial stability, payment resilience, and the role of intermediaries in the financial system.

Types of CBDCs

As central banks explore digital versions of sovereign currency, the conversation around CBDCs is increasingly focused on design choices rather than definitions. How a CBDC is structured — and who is permitted to use it — has important implications for payment efficiency, financial inclusion, privacy, and the role of commercial banks within the financial system.

Two dimensions are particularly relevant for investors and market participants. First is the intended user: some CBDC proposals are designed for everyday use by households and businesses, while others are limited to financial institutions and markets. Second is the operating model: CBDCs can be implemented with varying levels of involvement by central banks and commercial banks, which influences how closely a CBDC resembles today’s financial system and how disruptive it could be during periods of economic stress.

The tables below summarize these distinctions. Rather than signaling a single global model, they illustrate the range of approaches policymakers are considering — and the trade-offs embedded in each.

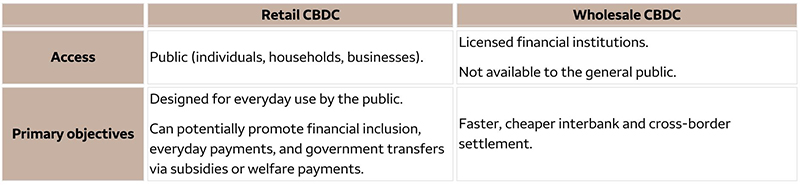

Retail versus wholesale CBDCs

| Retail CBDC | Wholesale CBDC | |

|---|---|---|

| Access | Public (individuals, households, businesses). | Licensed financial institutions. Not available to the general public. |

| Primary objectives | Designed for everyday use by the public. Can potentially promote financial inclusion, everyday payments, and government transfers via subsidies or welfare payments. | Faster, cheaper interbank and cross border settlement. |

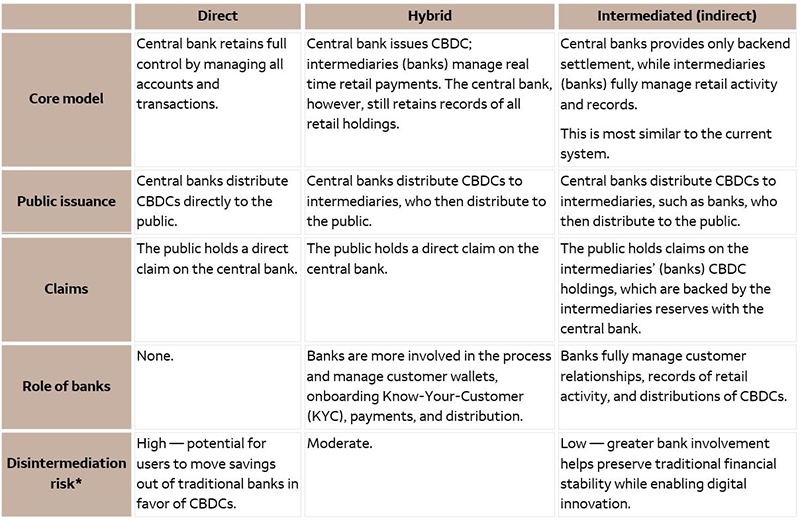

| Direct | Hybrid | Intermediated (indirect) | |

|---|---|---|---|

| Core model | Central bank retains full control by managing all accounts and transactions. | Central bank issues CBDC; intermediaries (banks) manage real time retail payments. The central bank, however, still retains records of all retail holdings. | Central banks provides only backend settlement, while intermediaries (banks) fully manage retail activity and records. This is most similar to the current system. |

| Public issuance | Central banks distribute CBDCs directly to the public. | Central banks distribute CBDCs to intermediaries, who then distribute to the public. | Central banks distribute CBDCs to intermediaries, such as banks, who then distribute to the public. |

| Claims | The public holds a direct claim on the central bank. | The public holds a direct claim on the central bank. | The public holds claims on the intermediaries’ (banks) CBDC holdings, which are backed by the intermediaries reserves with the central bank. |

| Role of banks | None. | Banks are more involved in the process and manage customer wallets, onboarding Know-Your-Customer (KYC), payments, and distribution. | Banks fully manage customer relationships, records of retail activity, and distributions of CBDCs. |

| Disintermediation risk* | High — potential for users to move savings out of traditional banks in favor of CBDCs. | Moderate. | Low — greater bank involvement helps preserve traditional financial stability while enabling digital innovation. |

Potential benefits

A frequently cited benefit of CBDCs is their ability to promote financial inclusion. In regions where access to traditional banking services is limited, CBDCs distributed through mobile devices can provide a low-cost entry point into the formal financial system. Pilot programs in emerging market countries have demonstrated how CBDCs can be used for government disbursements in areas with minimal banking infrastructure.3

CBDCs may also enhance the effectiveness of monetary policy. In principle, central banks could deliver policy actions — such as targeted transfers or stimulus payments — directly to households and businesses. This could reduce the reliance on commercial banks as intermediaries and shorten the lag between policy decisions and their impact on the real economy.

Key use cases

Payment and cross border settlement modernization

Several central banks — particularly in Asia and the Middle East — are pursuing CBDCs to modernize cross border payments. The mBridge initiative connects central banks in China, Hong Kong, Thailand, the UAE, and Saudi Arabia, enabling direct settlement without relying on the SWIFT network.4,5

Unlike SWIFT transfers, which can take 2 – 5 days and incur fees of 5% – 10%, mBridge aims to reduce settlement time and costs through shared digital payment rails. Though in its developing stage as of January 2026, the platform had processed more than $55.5 billion in transactions, with the digital yuan accounting for the majority of volume.6 This remains a tiny fraction compared to SWIFT’s $300 billion in daily transactions. Additionally, some countries also view alternative settlement infrastructures as a way to reduce dependency on existing payment networks, particularly in an increasingly fragmented global financial system.. For example, if two countries accept each other’s CBDC’s as forms of payment, they may be able to continue transacting with one another — even if sanctions are imposed by other countries that would otherwise limit them from using the traditional SWIFT payment system.

Global landscape and country examples

As of 2025, more than 134 countries — representing approximately 98% of global gross domestic product — are engaged in some form of research, experimentation, or early development related to CBDCs,7 as most projects remain in exploratory or pilot phases. One of the most advanced examples is China’s digital yuan (e CNY), which represents the largest CBDC pilot globally. Although adoption has been slower than initially anticipated, recent initiatives — including interest bearing features and expanded participation by financial institutions — aim to increase usage.8 In contrast, the United States has adopted a more cautious approach. Legislative developments, including the Anti-CBDC Surveillance State Act, reflect concerns about privacy and government overreach. As a result, U.S. efforts are focused primarily on wholesale CBDC research and cross border settlement initiatives.9

The European Central Bank continues to advance its digital euro project, emphasizing privacy protections and holding limits to mitigate financial stability risks.10 The Bank of England is similarly proceeding cautiously, evaluating a digital pound that would complement rather than replace existing payment methods.11 In emerging markets, several countries — including Nigeria, The Bahamas, and Jamaica — have already launched retail CBDCs, primarily to support financial inclusion and reduce cash handling costs.12

Risks and challenges

Despite their potential benefits, CBDCs pose several risks. One of the most prominent concerns relates to financial surveillance and privacy.13 Unlike physical cash, CBDCs can generate detailed transaction records. Without robust legal and technical safeguards, this information could be used in ways that extend beyond financial crime prevention, potentially undermining individual privacy and public trust.

Another challenge comes from the programmable nature of CBDCs. While features like spending limits or expiration dates can help governments manage economic activity and be effective policy tools, they could have the potential restrict how people use their own money. This raises concerns about personal financial freedom and highlights the need for clear rules and strong oversight.

CBDCs may also affect the banking system. If people choose to keep their money as CBDCs instead of depositing it in commercial banks, banks may have less money available to lend. This problem could become more serious during times of financial crisis, when CBDCs might seem safer than bank deposits.

Finally, there are legal issues to consider. In many countries, laws related to CBDCs — such as who is responsible for mistakes, whether CBDCs count as legal tender, and how transaction data should be protected — are still unclear. Addressing these legal and regulatory challenges is essential before CBDCs can be widely adopted.

The future of CBDCs

Interest in CBDCs continues to build globally as policymakers explore how money and payments may evolve in an increasingly digital economy. While most CBDCs are still in pilot or early development stages, ongoing experimentation is helping central banks better understand their potential role over time. Looking ahead, broader adoption will likely depend on coordination across countries, clearer policy frameworks, and thoughtful system design that works alongside existing financial institutions. Collaboration through international bodies such as the Bank for International Settlements, the International Monetary Fund, and the G20 could play an important role in shaping common standards and promoting cross border compatibility. If these efforts continue to progress, we believe CBDCs may gradually become a meaningful complement to today’s payment systems and financial infrastructure.

1 For a complete introduction to Bitcoin and Ethereum please see Wells Fargo Investment Institute’s report, “Bitcoin and Ethereum – What’s the difference?” October 16, 2025.

2 Distributed ledger technology is a decentralized and digital system used to record transactions and data across multiple computers. For a complete introduction please see Wells Fargo Investment Institute’s report, “Blockchain technology basics,” November 13, 2025.

3 “RBI’s offline digital rupee is here: Pay with e-rupee even without interest,” IBEF, October 14, 2025.

4 “What to watch as China prepares its digital yuan for prime time,” Atlantic Council, January 15, 2026.

5 “Project mBridge: connecting economies through CBDC,” BIS, October 26, 2022.

6 “China-led cross-border digital currency platform sees surge,” Reuters, January 16, 2026.

7 Central Bank Digital Currency Tracker. Atlantic Council, July 2025.

8 “What to watch as China prepares its digital yuan for prime time,” Atlantic Council, January 15, 2026.

9 “What does Trump’s CBDC ban mean for Digital Payments?” Juniper Research, February 2025.

10 “Progress on the digital Euro,” European Central Bank, data accessed as of April 14, 2026.

11 “The digital pound,” Bank of England, data accessed as of April 14, 2026.

12 “Central Bank Digital Currency Tracker,” Atlantic Council, July 2025.

13 “Central Bank Digital Currency Data Use and Privacy Protection,” IMF, April 2024.

Risks Considerations

This report is being provided for educational and informational purposes only and does not constitute a recommendation, solicitation, or offer to buy or sell any security, digital asset, financial instrument, or investment strategy. It is not intended to provide investment, legal, accounting, or tax advice.

References to central bank digital currencies (CBDCs), digital assets, payment systems, or related technologies are not intended as investment endorsements. CBDCs are issued and governed by sovereign authorities and are not currently available as investment products for U.S. retail investors. Any discussion of potential benefits or risks reflects general observations and does not imply suitability for any particular investor.

General Disclosures

Global Investment Strategy (GIS) is a division of Wells Fargo Investment Institute, Inc. (WFII). WFII is a registered investment adviser and wholly owned subsidiary of Wells Fargo Bank, N.A., a bank affiliate of Wells Fargo & Company.

The information in this report was prepared by Global Investment Strategy. Opinions represent GIS’ opinion as of the date of this report and are for general information purposes only and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally. GIS does not undertake to advise you of any change in its opinions or the information contained in this report. Wells Fargo & Company affiliates may issue reports or have opinions that are inconsistent with, and reach different conclusions from, this report.

The information contained herein constitutes general information and is not directed to, designed for, or individually tailored to, any particular investor or potential investor. This report is not intended to be a client-specific suitability or best interest analysis or recommendation, an offer to participate in any investment, or a recommendation to buy, hold or sell securities. Do not use this report as the sole basis for investment decisions. Do not select an asset class or investment product based on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs and investment time horizon. The material contained herein has been prepared from sources and data we believe to be reliable but we make no guarantee to its accuracy or completeness.

Wells Fargo Advisors is registered with the U.S. Securities and Exchange Commission and the Financial Industry Regulatory Authority, but is not licensed or registered with any financial services regulatory authority outside of the U.S. Non-U.S. residents who maintain U.S.-based financial services account(s) with Wells Fargo Advisors may not be afforded certain protections conferred by legislation and regulations in their country of residence in respect of any investments, investment transactions or communications made with Wells Fargo Advisors.

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC, Members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company.